2024 Financial Planning Tips for Private Practitioners

Unlock the key to financial success with our exclusive guide for private practitioners. Gain insights to enhance your 2024 financial planning.

As we welcome the beginning of a new year, business owners should take proactive steps to fine-tune their financial strategies. It is especially vital for private practitioners in 2024—when the healthcare landscape is likely to be more competitive than ever before.

For a successful year, it's crucial to focus on actionable steps that help achieve financial goals. We've outlined some practical tips to help private practitioners manage their finances better. By taking these steps, you can ensure your business is financially stable and well-positioned to thrive in the years ahead.

Tip 1: Regularly Update Billing Codes

Keep abreast of the latest ICD-10 codes. By doing so, you can mitigate the risk of claim denials and reduce the time it takes to receive reimbursement. Additionally, staying on top of the latest codes can help you provide better patient outcomes by accurately documenting their diagnoses and treatments.

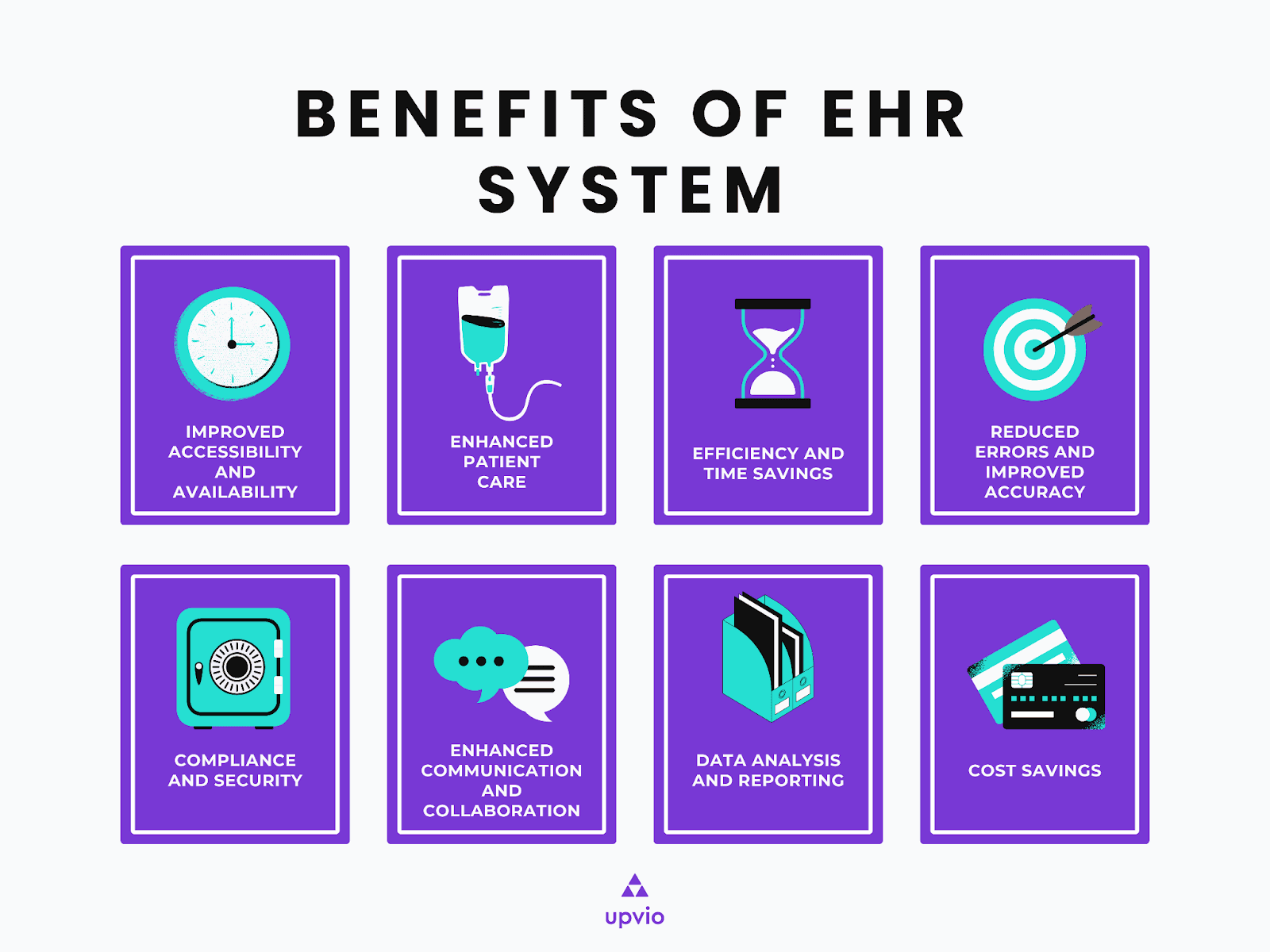

Tip 2: Implement a Robust EHR System

Investing in an Electronic Health Record (EHR) system with robust financial software integration capabilities is highly recommended. Such a system can significantly streamline billing processes and help to ensure accurate reporting.

By integrating with financial software, an EHR system can automatically gather billing information and generate invoices, reducing the need for manual data entry and speeding up the billing process. It can result in faster payment processing and improved cash flow for healthcare providers.

Moreover, an EHR system with financial software integration can help minimize errors, discrepancies, and confusion. It can automatically catch billing mistakes or discrepancies and alert healthcare providers, reducing the risk of costly billing errors.

Further Reading:

What Is the Difference Between CPT and ICD Codes?

Tip 3: Conduct Regular Financial Audits

Regular reviews conducted either monthly or quarterly can play a crucial role in identifying any financial discrepancies that may have occurred within an organization. Such reviews can help prevent potential financial losses while ensuring that the revenue generation is optimized to its fullest potential. Additionally, understanding what business expenses are tax deductible during these audits can help maximize savings. Identifying deductible expenses, such as office supplies, staff training, or software subscriptions, ensures that you are not leaving money on the table when filing taxes.

Tip 4: Set Clear Patient Payment Policies

Establishing transparent financial responsibilities for patients is crucial in ensuring economic goals. Setting realistic expectations and facilitating smoother transactions provide patients with a clear understanding of their financial obligations and can avoid any unpleasant surprises later on.

Additionally, transparent financial responsibilities can help build trust between healthcare providers and patients, which is essential for the overall success of medical treatment.

Tip 5: Stay Updated with Medical Schemes and Private Payer Policies

It's also essential to keep yourself updated about the changes in reimbursement and billing policies, as they can affect your private practice's financial performance.

One mistake in this area can prove to be quite expensive. Therefore, staying informed and aware of the latest policies is one of the best ways to avoid costly errors and maximize revenue.

Tip 6: Invest in Continuous Staff Training

One effective way to optimize your medical practice's billing and coding procedures is to provide your team with ongoing education and training.

It can include training on accurately coding medical procedures, properly documenting patient information, and navigating the complexities of insurance billing.

Ongoing education can also help your team stay up-to-date with changes in regulations and compliance requirements, which is essential for maintaining a financially healthy medical practice.

Tip 7: Create a Contingency Fund

A financial cushion can provide your practice some buffer in unforeseen circumstances, such as a sudden drop in revenue or unexpected expenses. By setting aside some funds, you can ensure continued business during difficult times.

Remember, it's always better to be prepared and proactive rather than reactive when it comes to your finances.

Bottomline

With careful 2024 financial planning, this year can mark tremendous success for private practitioners like you, ensuring financial health and resilience in the face of uncertainties.

Find more practical and helpful tips to improve your private practice.

More related content you might find useful:

Discover how Vitals AI captures 20+ health markers in a few seconds.

Dive deeper with Is Practice Management Software Suitable for Small Mental Health Practices?.

Read more in Why Multimodal Matters: Fusing Voice, Face, Language, and Vitals.

Read more in Understanding PHI: Protected Health Information Explained.

Dive deeper with Understanding the Role of Practice Management Software.